If you’re like most homeowners, you probably went through a local bank to get a mortgage. After a month or two, you probably then received a letter saying your mortgage had been sold and to start making payments to the new lender. This scenario is very common and is an accepted practice within the banking industry. But did you know that homeowners can do the same? That's right! You can sell your mortgage just like a big bank! This article will show you how to sell your mortgage and explain the benefits Good Vibes Homebuyers delivers when we buy house’s subject to the existing mortgage.

What’s in it for you:

Selling “subject-to” the existing mortgage means selling your home and keeping the existing mortgage in place. You get paid for your equity, and Good Vibes Homebuyers (GVH) takes over the remaining mortgage balance. As the new owner, GVH makes the monthly mortgage payments, pays the property taxes, insurance, HOA dues, and all other obligations related to the home. Selling subject-to your existing mortgage is quite simple and is a valuable choice for homes and homeowners in nearly all situations.

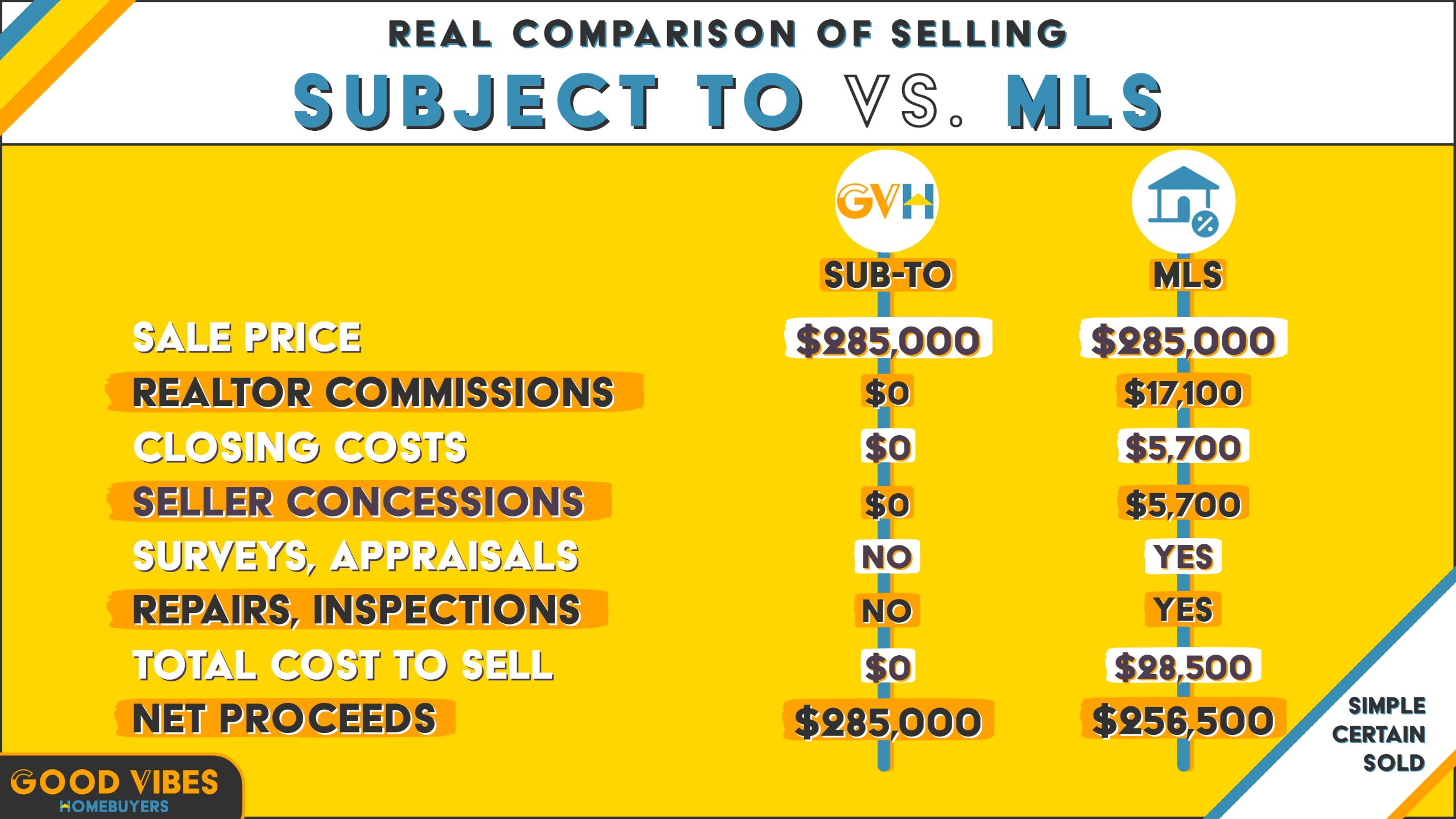

When selling subject-to the existing mortgage, Good Vibes Homebuyers is able to give sellers like you more money because you aren’t having to pay traditional costs like realtor commissions (6% savings), closing fees (2% savings), and seller concessions (2% savings). When we buy your home subject-to its existing mortgage, we pay all closing costs and buy the home in “as-is” condition, which means you have zero repair costs (1+% savings).

Because GVH avoids future financing costs when you sell your mortgage, we pass that cost savings onto you, which means more money in your pocket. At closing you receive a direct cash payment which is based on your home’s condition, mortgage payment, equity, and the estimated monthly rent (learn about our home valuation process).

Below is a real comparison of a subject-to the existing mortgage offer that was accepted by a homeowner who sold their mortgage to GVH:

The biggest perk of selling your home subject-to is that it reduces transactional costs for both buyer and seller. This means 3 things: (1) sellers have zero expenses, (2) GVH has zero financing costs, and (3) GVH passes its cost savings onto the seller. Other reasons for selling your house subject to the existing mortgage are situations where homeowners (a) need fast cash, (b) are behind on mortgage payments (c) are facing foreclosure, (d) have little or no equity, (e) want to improve their credit, and (f) want to get the most money possible.

No matter the method for selling your home, each has their benefits and drawbacks. Selling subject-to is no different. In most situations, however, the benefits outweigh the disadvantages. So, what are the pros and cons of selling a house subject to?

a. Due on sale clause. Every mortgage has a provision that is commonly referred to as the due-on-sale clause which says that the lender has the right, but not the obligation, to call the mortgage due upon a change in ownership. On the surface, this seems quite scary; however, banks rarely, if ever, invoke this clause. Consider the advice of David Willis, a highly regarded Texas real estate attorney:

“Due-on-sale merely enables the lender to choose to act - if the seller transfers title, then the lender may demand that the mortgage be paid off. But the lender would have to decide that such action is in its best interest, and most balk at accelerating an otherwise performing loan. Experience shows that the risk of acceleration is small while the loan remains current.” (Good Vibes Homebuyers will catch-up all missed payments to bring your loan current.)

This clause has never been invoked on any of the homes we’ve bought subject-to. In fact, we’ve never heard of this happening in Texas.

b. The mortgage is a VA Loan. Although with VA loans you absolutely can sell a home subject to its existing mortgage, one must note that it could impact your ability to obtain another VA loan in the future. To stay within the VA mortgage entitlement limit, the total amount of all VA loans in the name of a single individual cannot exceed $647,200. Even though obtaining a 2nd VA loan is possible, we must reiterate that there are specific criteria that must be met and therefore we encourage homeowners to speak with a reputable VA lender or to investigate other low-cost mortgage options like Fannie Mae, Freddie Mac, and FHA loans.

c. The mortgage stays in your name. For some homeowners, this may not be ideal while for others, it’s extremely beneficial. Homeowners who intend to buy a new home after selling their old home, may not be immediately eligible for a new mortgage if they do not meet standard underwriting requirements. Conversely, homeowners with poor credit will see a boost in their credit score as GVH continues to make the monthly mortgage payments (GVH has never missed nor made a late mortgage payment).

a. Make more money: In most situations you will make more money than you would with a traditional sale. Here’s why: (i) you pay no closing costs, (ii) GVH pays no financing costs, and (iii) GVH passes its savings on to you. In short, you have no expenses, our costs are reduced, and therefore we can pay you more.

b. Make money even with no equity: Homeowners with less than 11% equity who try to sell traditionally will have to bring money to the closing table. When selling your home subject to its existing mortgage where you have 11% or less in equity, GVH can still pay you up to $10,000.

c. Your mortgage is brought current: If you’re behind on mortgage payments, Good Vibes Homebuyers will catch-up all missed payments so that your loan is brought current. This is a critical step to improving your credit.

d. Fastest closing: Homeowners who need fast cash or a quick closing can sell their home subject to the existing mortgage in as little as 1 day. Closing a traditional sale averages 40-50 days.

e. No inspections, repairs, surveys, or appraisals: You went through this process when you bought the home. Because you already have a loan in place, there is no need to repeat these steps, so closing a subject to mortgage is very simple!

f. Easiest closing: Our team provides full-service sell your mortgage solutions meaning we complete all tasks needed to close. On occasion, you will need to provide basic information but your most time intensive obligation will be signing closing documents and collecting your cash.

Good Vibes Homebuyers has helped many homeowners navigate through and out of many situations by using our sell your mortgage solution. With this experience we have fielded many questions from homeowners, and below we discuss and answer these common questions about selling a home subject to.

You can get a new mortgage for a new home as fast as the day after selling your old house subject to. Doing so is dependent on your personal credit and lender requirements. Even if you have subpar credit, the good news is - all is not lost.

Once Good Vibes Homebuyers takes ownership of your old mortgage, the title is transferred out of your name, and therefore, the mortgage no longer counts against your debt-to-income ratio. Moreover, because we’ve been making the mortgage payments on time and in full, your credit will improve. At this point, sellers need only to meet standard underwriting requirements.

Texas Property Code Section 5.016 allows homeowners to sell your home with an existing mortgage that will not be paid off, provided the seller provides the buyer with a disclosure notice. GVH will gather the information needed for the notice which includes the mortgage terms, its unpaid balance, interest rate, and monthly payment. Providing GVH with a copy of your most recent mortgage statement allows us to complete this disclosure on your behalf.

When we buy homes subject to its existing mortgage, our commitment is to continue to pay the mortgage (and all other obligations related to the home) until the mortgage balance hits zero. Nevertheless, we are willing to negotiate a timeframe in which we are required to pay off the existing mortgage. Although there is no guarantee of the below occurring, there are a couple scenarios where the mortgage you sold would be paid off early.

a. The 1st scenario where the mortgage would not stay in your name is the home is sold on the MLS which could happen as soon as the home reaches 25% equity. In this scenario, the sale proceeds would be required to pay off the existing mortgage in full.

b. The 2nd scenario where the mortgage would not stay in your name is once the home achieves 50-55% equity or to take advantage of lower interest rates. In this scenario, GVH would refinance out of the mortgage you sold, and the new lender would pay off the subject to mortgage in full.

We’re not breaking news here - we invest in real estate to make money which is achieved by renting homes for cash flow and/or building equity in them over time. In a subject to transaction, we are paying you cash for the equity you’ve built meaning that we have zero equity at our purchase. As such, our focus is on generating a return through renting the home.

There is no one-size-fits-all approach but the simplest test for a “doable” deal when we buy houses subject to the existing mortgage is that the monthly rent must be greater than the monthly mortgage payment. In today’s market this has become challenging which demands that we consider the factors that make your home unique. These include characteristics like stainless steel appliances, updated bathrooms and kitchen, location, the neighborhood, and your home’s overall condition. In an ideal world, these factors align to produce monthly rents that exceed the monthly mortgage payment.

Because we do not live in an ideal world, GVH uses the above characteristics to predict the property’s rate of appreciation which is a notable factor in determining if a home can be sold subject to its existing mortgage. In short, we trade cash flow while betting on appreciation. In so doing, we are open to losing about 1% in annual cash flow relative to the home’s value. For instance, if the market value is $300,000, we can probably live with a -$3,000 annual loss. But if the monthly rent equals or is greater than the monthly mortgage payment, you may be saying, "that doesn’t add up, you should be making money!” Many homeowners don’t consider the cost of owning rental real estate, which we call V.C.R.T.I.P. (Vacancy. Capital expenditures. Repairs. Taxes. Insurance. Property management). Below is a recent, real-life example of a house we bought subject to the existing mortgage:

In nearly all cases, when we buy homes subject to, GVH loses money during its first 3-5 years of ownership.

Since the mortgage remains in the seller’s name, safeguarding and improving the seller’s credit and financial standing is of paramount importance. To that end, sellers receive the following protections:

a. Bank draft: Our commitment is to pay in-full each month the mortgage and all other obligations related to the home. At closing, a limited power of attorney will be signed giving GVH the right to set up a connection with the mortgage company so that payments can be made via ACH draft from our bank account. If desired, we will email confirmation of payment to you each month. Furthermore, after selling your home subject to the existing mortgage, you will retain access to your online account and may contact the lender directly to verify the mortgage you sold is current.

b. Multiple assets we can barrow against: Good Vibes Homebuyers maintains a cash account exceeding $750,000 and owns multiple properties with significant equity that we can borrow against to meet our financial obligations to you.

c. Cash account: Although unheard of, should the lender choose to call the loan due, our secure financial position guarantees that we’ll be able to meet our financial responsibilities to you. Furthermore, when renters of the house you sold subject to the existing mortgage do not pay rent, our cash account guarantees that the mortgage payment will continue being made.

d. Credit report: If desired, Good Vibes Homebuyers will provide you with a recent personal credit report of its managing members who have maintained a minimum credit score of 785 since 2016.

e. You can foreclose on us: When someone doesn’t make their mortgage payment the bank can take back the home. And remember that when you sell your mortgage you become the bank? At closing you can elect to receive a promissory note which is a signed document that promises to pay the balance of the existing mortgage. You can also elect to receive a deed of trust, which is a document that enforces the promissory note.

With these documents, if GVH does not make the mortgage payments (we guarantee all obligations will be paid in full, on time), you can foreclose on us and take back the property! Although this situation may not be ideal for you or us, it wouldn’t be terrible for you, either.

Why? You would keep the cash that we paid you at closing, and you would get to capitalize on any improvements and appreciation that have taken place since you sold your home’s mortgage to us. We obviously do not want to be foreclosed upon, so we are highly incentivized to follow-though on all our commitments to you.

When you sell your home’s mortgage to GVH, we close subject to transactions with a real estate attorney who is knowledgeable in the legalese of buying and selling homes subject to the existing mortgage. We pay all closing costs and can close in as little as 1 business day. At this link you can find the contact information of the real estate attorney we regularly use to handle the subject to closing process.

1. What will you need to provide me with offers to sell my home subject to its mortgage?

Just 3 things: (i) your monthly mortgage payment (ii) whether your mortgage payment includes escrow for property taxes and insurance; and (iii) the estimated remaining mortgage balance. Once received, we will provide you with solid offers that are contingent on visiting the home to determine if repairs are needed. If necessary, our subject to the existing mortgage offers will be offset by the cost of repairs.

2. What are the tax implications when I sell my house subject to the existing mortgage?

Once the title of the property is transferred out of your name, you no longer have any tax obligations or receive the tax deductions associated with the home.

3. How long does it take to close when I sell my mortgage?

GVH can close in as little as 1 business day. The average time to close a subject to transaction is 4 business days.

With our sell your mortgage solution most homeowners will get more money than selling on the MLS. You avoid showings, staging, and all the hassles and headaches of a traditional sale. The Good Vibes Homebuyers team provides full-service solutions that pay you cash in as little as 1 day and we will even pay up to $10,000 for homes with no equity. We cover all closing costs, will bring your mortgage current, and can even help you find and move into your next place. It’s time for you to thrive with Good Vibes Homebuyers! Contact us today!

Free closing costs. Free Local Move. Zero fees. Sell in 5 days. Sell and stay for 180 days. No equity? Still get $10,000 cash!

Picking the wrong investor can leave you scrambling & empty-handed. Learn how to spot the bad from good investors & see the top reasons to pick Good Vibes Homebuyers.

What sounds better - winning or losing? Home investors don't want you to know these 4 magic negotiation tactics because you'll kick their butt and come out a winner!

Good Vibes Homebuyers might be the perfect option for many Texas property owners needing to sell a house. Ask yourself these questions to see if our investors are right for you.